Retirement Planning Framework

Understanding how structured portfolio design can support long-term retirement income.

Structuring Retirement Income

Retirement planning is often viewed primarily as the process of building a sufficient corpus. In practice, however, the sustainability of retirement depends just as much on how that corpus is structured to generate income over time.

Retirement portfolios may need to support income for 25–35 years or longer, while also navigating market fluctuations and rising living costs. Because of this, many retirement frameworks focus on aligning investment horizons with spending horizons, ensuring that short-term income needs are not dependent on market movements.

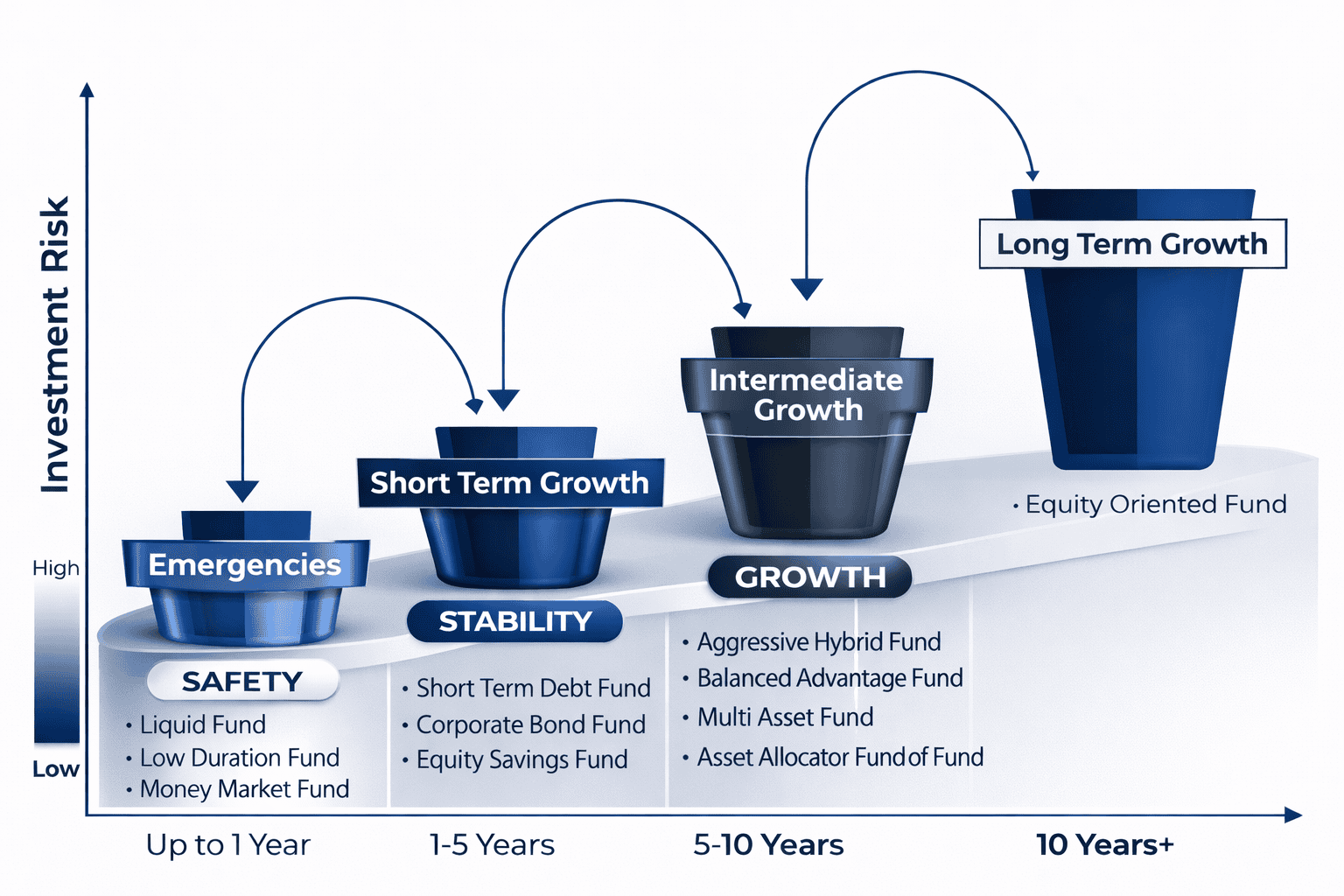

How the Buckets Work Together

Retirement planning is often viewed primarily as the process of building a sufficient corpus. In practice, however, the sustainability of retirement depends just as much on how that corpus is structured to generate income over time.

Retirement portfolios may need to support income for 25–35 years or longer, while also navigating market fluctuations and rising living costs.

Because of this, many retirement frameworks focus on aligning investment horizons with spending horizons, ensuring that short-term income needs are not dependent on market movements.

Situations Where This Approach May Be Suitable

- Managing income during market volatility

- Reducing the need to sell assets during downturns

- Aligning investments with time horizons

- Balancing safety with long-term growth

- Supporting inflation-adjusted income

- Creating a clearer structure for retirement withdrawals

Retirement portfolios often need to balance several priorities — generating regular income, managing market volatility and maintaining purchasing power over time. A bucket-based approach may be suitable for some retirees because it separates assets according to time horizon and purpose, which can help structure how retirement income is generated and sustained over the years.

A Conceptual Framework

The bucket strategy is one of several approaches used in retirement planning to structure portfolio withdrawals and manage income sustainability. Actual portfolio design may vary depending on individual financial circumstances.

Educational Disclaimer

Succinct FinTech Services Private Limited is a SEBI Registered Investment Adviser. The information presented here is intended for educational purposes only and does not constitute investment advice or solicitation.